My initial introduction to retirement planning was at the age of 23 when I started my first job as a Pharmacist in Boston, MA. I remember receiving a paper memo (yeah I’m that old) in my mailbox asking me to make my 401k elections. I made random selections based on the coolness of the investment fund name and moved on. After several years and several prescriptions later, I stumbled upon a completely different retirement account that I was not taking advantage of….the Individual Retirement Account (IRA).

What is an Individual Retirement Account?

An IRA is an investment account that individuals can use to tuck away money for retirement. The money can be invested in the stock market and grows tax-free until the funds are withdrawn in retirement. The contribution into the IRA may yield a deduction on tax returns but this depends on income levels and ability to contribute to other qualified retirement plans. For most employed professionals (Pharmacists, Physicians, etc), the contribution is not deductible on taxes but this does not prohibit the ability to contribute to an IRA. See 2021 IRA Deduction Limits HERE.

The 3 Major Types of IRAs:

- Traditional IRA – Contributions are made with after tax money (i.e., money that you already paid payroll tax on) but may be deducted on your tax return depending on income level. Earnings grow tax-deferred until you withdraw the funds in retirement. The tax on the distribution in retirement is typically lower than the tax you’d pay in the prime of your career.

- Roth IRA – Contributions to this account are made with money you’ve already paid taxes on, the money grows tax-free, and the money is distributed tax-free in retirement. There are specific restrictions on this kind of IRA that prevents high-wage earners from contributing directly to the IRA. (High earners can use the Backdoor Roth conversion method to get around this restriction).

- Rollover IRA – This is similar to a traditional account however, the funds in this account have “rolled over” (transferred) from an employer-sponsored plan, such as a 401(k) or 403(b), into the IRA.

Roth IRA

The Roth IRA , initially called the “IRA Plus”, was an idea proposed by Senator Bob Packwood of Oregon and Senator William Roth of Delaware. It was established in the Taxpayer Relief Act of 1997 and provided the ability for Americans to make non-deductible contributions to a special IRA that could be used tax-free in retirement.

Advantages include:

- Tax-free retirement income

- Easy early access to money

- Not subject to RMDs (required minimum distributions)

- Passes on to heirs tax-free

- Available to any American with earned income

Disadvantages include:

- Taxes are paid upfront

- No tax deductions for contributions

- High earners can not contribute directly

- Individuals must setup the account on their own and not with an employer

What makes a ROTH so special?

The money within a Roth IRA grows tax free and can be distributed tax free! All interest, dividends, and capital gains are left in the account to compound over time without fear of the IRS taxing it in retirement. Even more, direct contributions to a Roth IRA can be removed at any time without penalty should you need the money before retirement age of 59.5 years. After the age of 59.5, contributions, conversions, and the earning can be withdrawn tax free. The account must be open for at least 5 years to take a qualified distribution. In addition, there are exceptions that permit the early withdrawal of the earnings before the age of 59.5. These include purchase of a first home (up to $10,000), for medical expenses greater than 7.5% of adjusted gross income, and to help pay for college expenses.

Qualifications to contribute to a ROTH IRA:

- You must have “Earned income” in the given tax year to contribute. This means you actually earned money from a job, side hustle, or small business. Earned income includes wages, tips, etc.

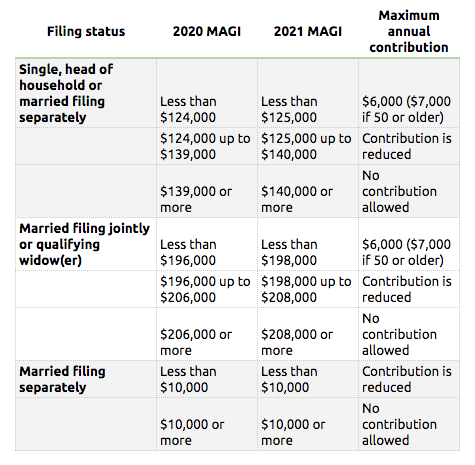

- The are Income limits to contribute directly to a Roth IRA: